Question 5:

PRACTICAL PROBLEM

Vishnu, Prabhakar and Krishna were partners in a business sharing profits and losses in the ratio of 3:1:1 respectively. Their Balance Sheet as on 31st March, 2012 was as follows:

Balance Sheet as on 31st March, 2012

Krishna died on 1st October, 2012 and the partnership deed provided that:

1) The deceased partner to be given his share of profit to the date of death on the basis of the profits of the previous year.

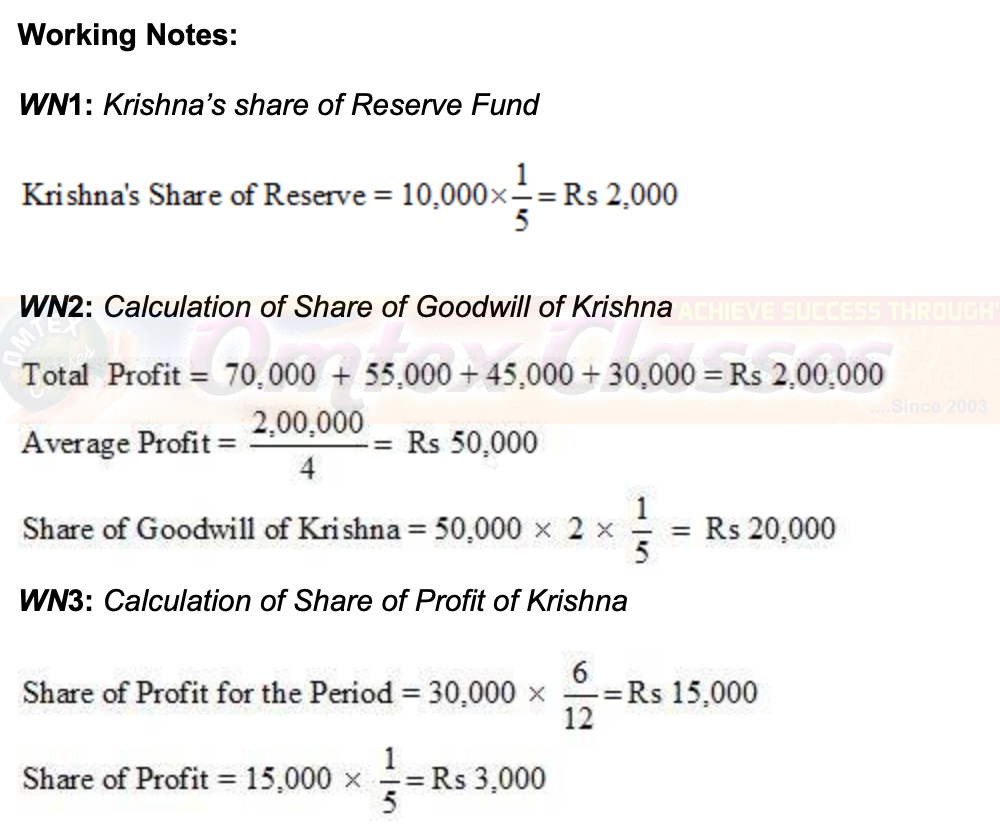

2) His share of goodwill will be calculated on two years purchase of average profit of the last 4 years. The net profit for last 4 years were Rs 70,000, Rs 55,000, Rs 45,000, Rs 30,000

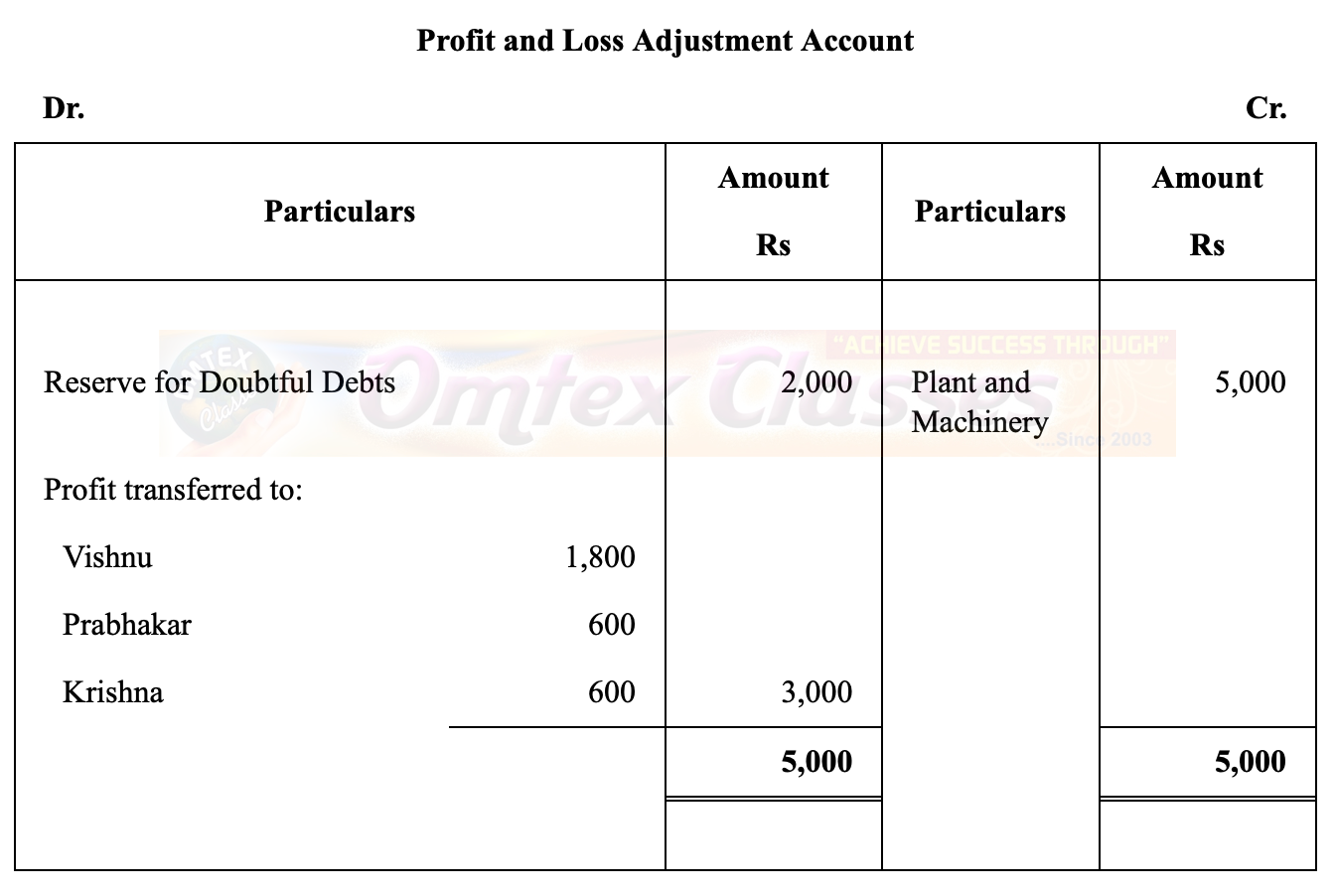

3) Plant and Machinery to be valued at Rs 40,000. Reserve for doubtful debts of Rs 2,000 to be created.

4) The drawings of Krishna upto the death amounted to Rs 20,000

5) Interest on capital at 10% p.a. is to be allowed and 6% p.a. to be charged on drawings. Both the interest should be calculated for 6 months.

Krishna died on 1st October, 2012 and the partnership deed provided that:

1) The deceased partner to be given his share of profit to the date of death on the basis of the profits of the previous year.

2) His share of goodwill will be calculated on two years purchase of average profit of the last 4 years. The net profit for last 4 years were Rs 70,000, Rs 55,000, Rs 45,000, Rs 30,000

3) Plant and Machinery to be valued at Rs 40,000. Reserve for doubtful debts of Rs 2,000 to be created.

4) The drawings of Krishna upto the death amounted to Rs 20,000

5) Interest on capital at 10% p.a. is to be allowed and 6% p.a. to be charged on drawings. Both the interest should be calculated for 6 months.

Prepare:

1) Krishna’s capital A/c and P/L Adjustment A/c

Note: As no information is given regarding the New Ratio of Vishnu and Prabhakar, hence, it is 3:1 and Gaining Ratio is same as the New Ratio.